Bear markets are not exceptions they are a structural feature of equity markets. Since 1928, the S&P 500 has spent approximately 40% of all trading days in some form of drawdown from a prior peak. The question is not whether the next decline will come, but whether you have a framework to navigate it.

Definition

A drawdown measures the decline in value of an investment from its most recent peak to its subsequent trough. For the S&P 500, drawdowns range from brief pullbacks lasting a few days to multi-year bear markets that erode a significant portion of portfolio value.

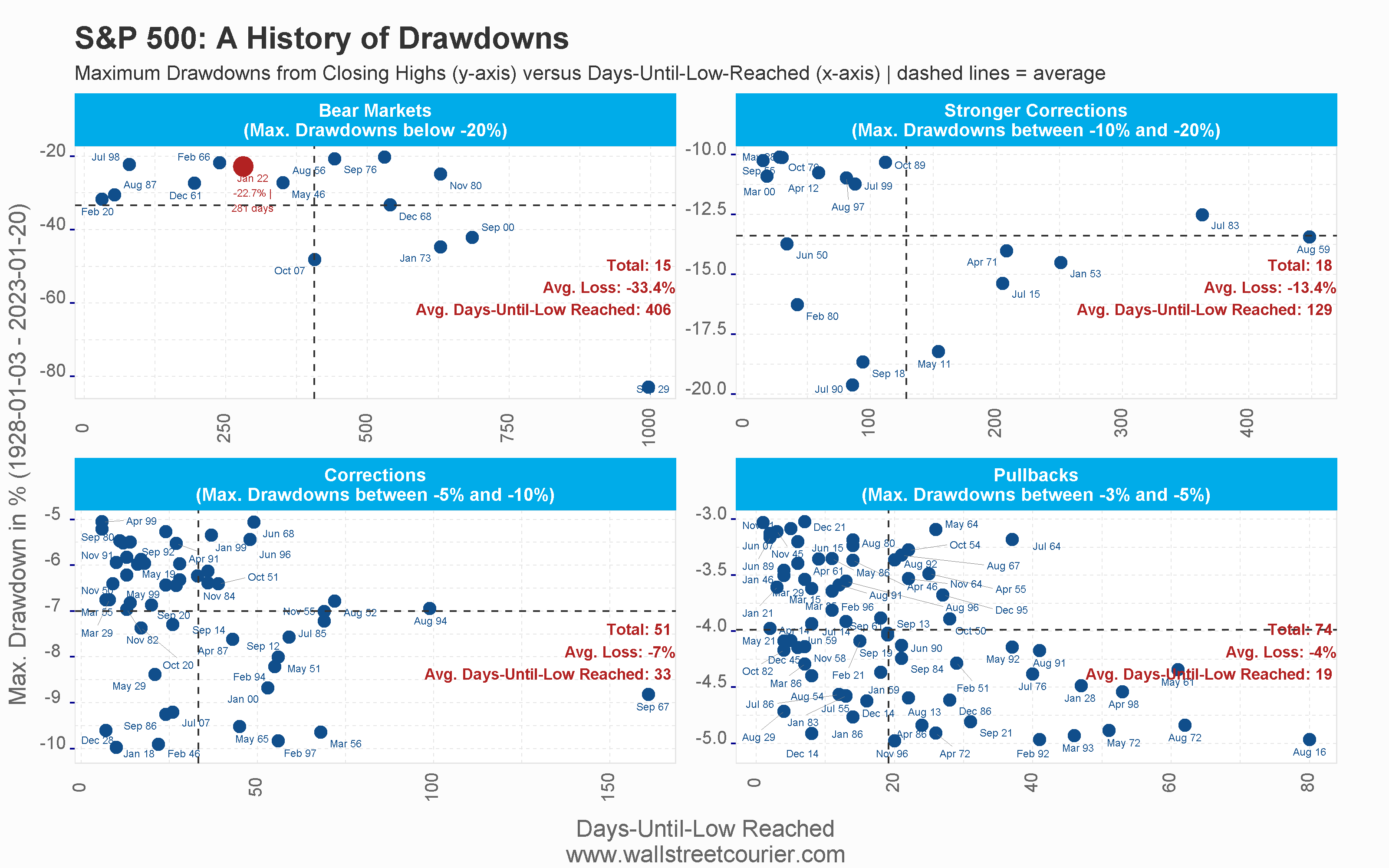

There are four commonly used severity categories. Bear markets are declines exceeding 20% from peak to trough. Stronger corrections are declines between 10% and 20%. Corrections are declines between 5% and 10%. Pullbacks are declines between 3% and 5%.

In short: A drawdown is not a sign that something has gone wrong. It is a normal, recurring feature of equity investing and understanding its historical frequency, severity, and duration is the first step toward managing it effectively.

WallStreetCourier analyzed all S&P 500 closing-price drawdowns from January 1928 through December 2023 a 95-year dataset covering every bear market, correction, and pullback across one of the longest available equity price histories. The data reveals how frequently severe market declines occur, and how long investors must typically endure them.

The chart below classifies every S&P 500 drawdown by severity category, with the average decline and average time to the final low marked for each group.

Since 1928, the S&P 500 has recorded 15 bear markets defined as peak-to-trough declines exceeding 20%. Collectively, these events account for 8,520 trading days, or roughly one quarter of the entire observation period. No investor with a meaningful time horizon can expect to avoid them.

The fastest bear market in recorded history was the 2020 COVID-19 crash, which reached a 34% trough in just 32 days. Black Monday in 1987 followed closely, bottoming in 54 days. At the other extreme, the Great Depression decline lasted 996 days and destroyed 82% of equity value. The 2008 Financial Crisis fell 48% over 407 days. The dot-com crash (2000–02) lasted 685 days with a 49% total loss.

| Category | Count | Avg. Decline | Avg. Days to Low | % of Total Period |

|---|---|---|---|---|

| Bear Market >20% | 15 | 33.4% | 406 days | ~25% |

| Stronger Correction 10–20% | 18 | 13.4% | 129 days | ~9.4% |

| Correction 5–10% | 51 | 7% | 33 days | ~4.9% |

| Pullback 3–5% | 74 | 4% | 19 days | ~4% |

Between the dramatic bear markets that dominate financial history lie a steady stream of less-severe drawdowns. Since 1928, stronger corrections (10–20% losses) have occurred 18 times, averaging 129 days to their lows. Standard corrections (5–10%) have occurred 51 times. Pullbacks (3–5%) a further 74 times.

Stronger corrections (10–20% decline): The longest ran from August 1959 to October 1960 448 days with a 13% total loss. The fastest reached its low in just 15 days (September 1955) and recovered to a new high within 34 days. These 18 events account for 3,286 days of market pressure, or about 9.4% of the full observation period.

Standard corrections (5–10% decline): The 51 standard corrections averaged a 7% decline over 33 days. One outlier a prolonged 1967 correction lasting 161 days skews the average; the median duration was closer to 26 days. Together these account for 1,701 days, or approximately 4.9% of the period.

Pullbacks (3–5% decline): With 74 occurrences, pullbacks are the most frequent category. The fastest lasted a single day (November 2021, 3% decline). The longest ran 80 days (August 2016, 4.9% decline). Investors should expect several pullbacks per year in typical market conditions.

See where the S&P 500 stands in today's market regime free, no credit card required.

Register FreeUnderstanding the history of drawdowns is the foundation. Navigating them in real time requires a strategy. The three approaches below represent distinct philosophies for managing downside risk each with its own requirements, tradeoffs, and evidence base.

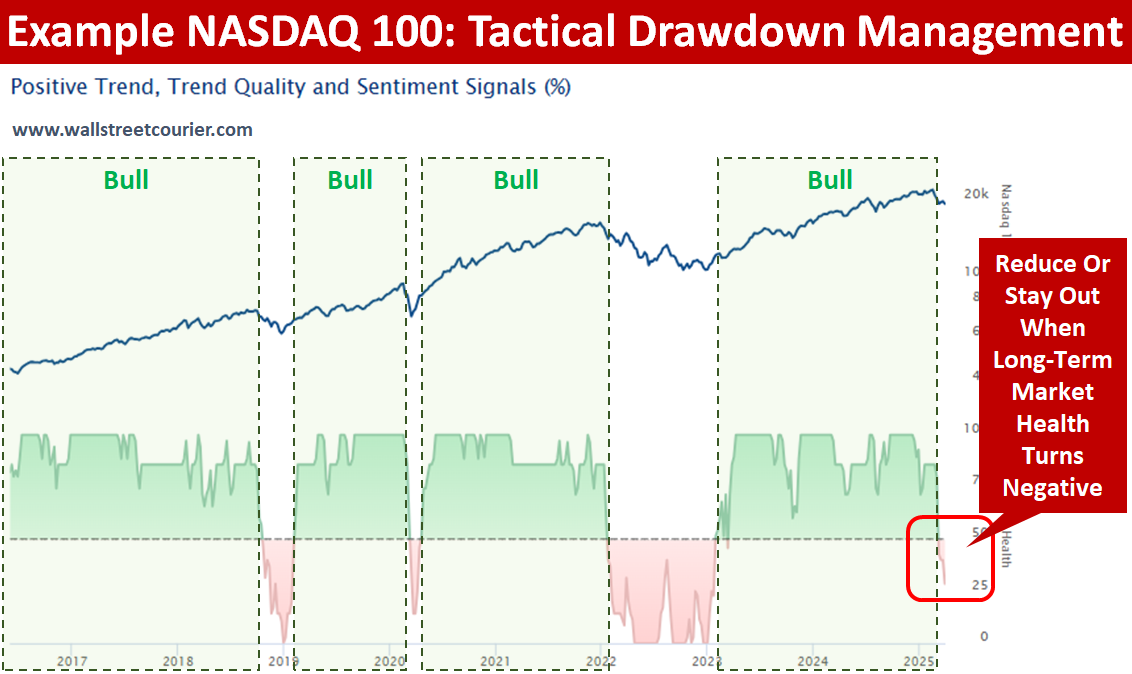

Tactical investing adjusts portfolio exposure based on measurable changes in market conditions trend strength, breadth, sentiment, and institutional positioning rather than maintaining a fixed allocation through every environment. The objective is not to predict market turning points, but to stay aligned with the prevailing regime.

When applied with discipline and driven by robust data, tactical management can reduce the depth of major drawdowns while still participating in bull market advances. The critical requirement is a structured, research-driven framework that removes subjective judgment from allocation decisions.

One evidence-based approach to tactical investing is the WSC Long-Term Market Health Indicator. This indicator aggregates dozens of time-tested metrics trend, market breadth, sentiment, smart money and dumb money positioning into a single structured signal. When the indicator is above zero, the majority of underlying metrics are aligned to the upside and the strategy favors staying invested. When it falls below zero, the balance of evidence warrants reducing exposure.

Tactical investing does not eliminate drawdowns it aims to sidestep the most damaging ones. As the chart above illustrates, avoiding exposure during the shaded periods of structural weakness would have reduced peak-to-trough losses significantly while maintaining full participation in bull market advances.

Diversification across asset classes equities, bonds, commodities, and alternatives has historically reduced portfolio volatility and cushioned drawdowns. A multi-asset approach smooths return profiles and provides a buffer when equity markets fall sharply.

However, traditional diversification is under pressure. In environments where equities and bonds fall simultaneously which has occurred with increasing frequency in inflationary and rising-rate regimes a 60/40 portfolio provides less protection than historical averages suggest. Correlations between major asset classes tend to spike precisely during the stress events investors most need protection from.

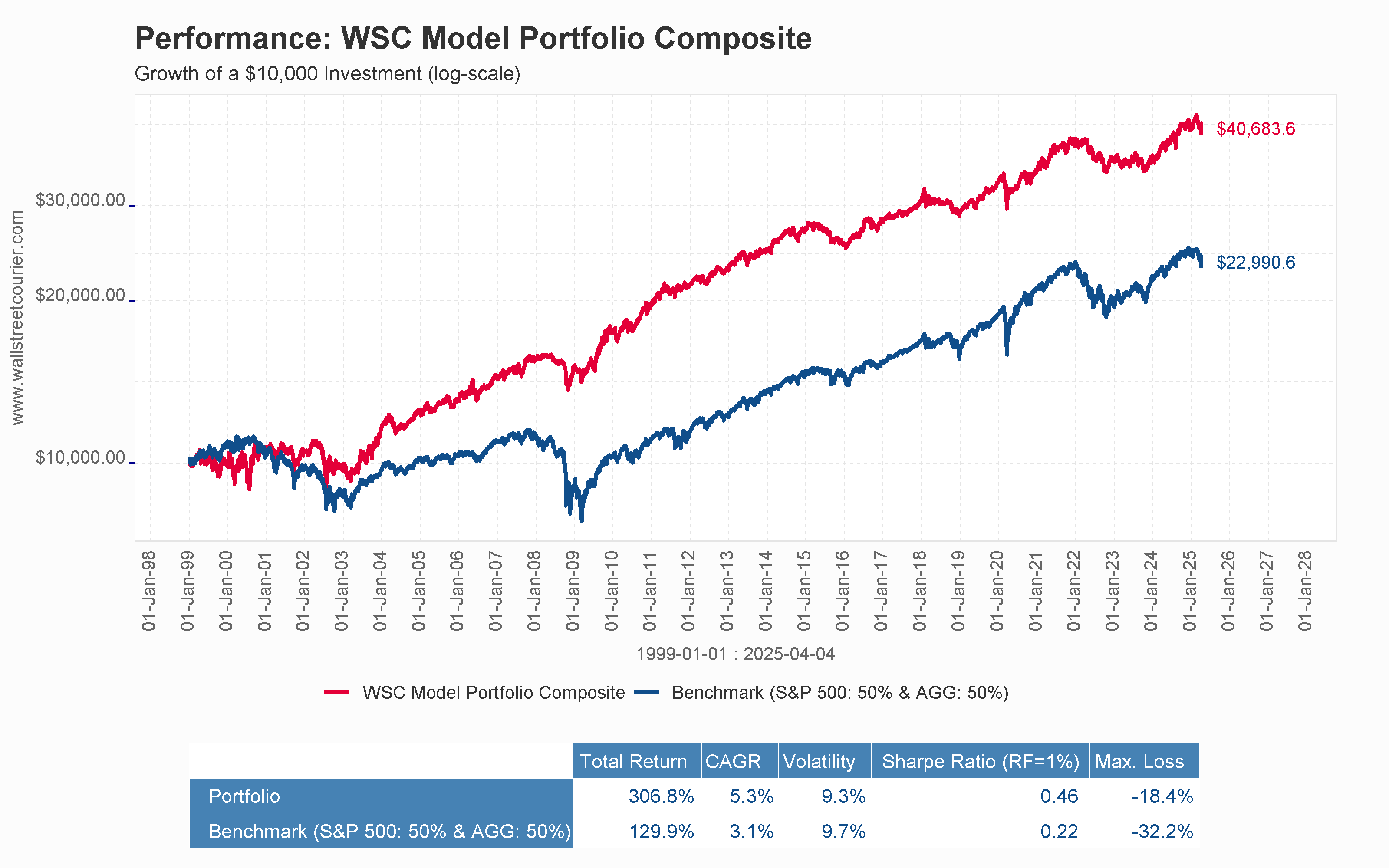

One response to this correlation challenge is to diversify not just across asset classes, but across complementary investment strategies and market regimes. This approach targets a portfolio with low correlation to any single asset class while maintaining consistent exposure to return premiums across different market environments.

The WSC Model Portfolio Composite is designed to achieve outstanding risk-adjusted returns across all market environments with minimal correlation to common asset classes by exploiting the diversification premium systematically. Since 1999 it has delivered a cumulative return of 370% against a 171% benchmark return, with a Sharpe ratio of 0.58 across the Dynamic Variance portfolio.

The buy-and-hold approach rests on the empirically supported belief that equity markets recover from every decline over a sufficiently long time horizon. It eliminates transaction costs, avoids market-timing errors, and benefits from the full compounding of long-term equity returns.

Its limitation is behavioral and financial: the historical data makes clear that staying invested through a bear market is far more demanding than most investors anticipate. A 33% average decline sustained over 406 days is not an abstract statistic it is a multi-year period during which significant real-world wealth is destroyed with no certainty of when recovery begins.

Buy and hold works for investors with long time horizons, genuine emotional resilience, and the financial capacity to avoid portfolio withdrawals during downturns. For most retail investors, a purely passive approach without any regime awareness exposes the portfolio to unnecessary depth and duration of drawdown. The historical data does not argue against buy-and-hold it argues for understanding the realistic demands of the strategy before committing to it.

The WSC Market Health Score classifies 29 global markets daily across six regime zones. Access one full market per week Morning Briefing, Smart Money Flow Index, and Market Regime Report at no cost. Bloomberg data provider since 2003.

You are currently viewing a placeholder content from X. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information